Home or investment, climate change is not your property's friend

Roughly two thirds of Australians own a property, with or without a mortgage. The rest rent. We all need to note the risks climate change throws at real estate.

By now you’ve seen the intro, a bit about me, and a summary of the data leading me to my conclusion climate change will take a wrecking ball to your wealth.

Let’s dive deeper into the threats to property…

It all starts with insurance

I’ve mentioned this in the previous blogs, but I’ll say it again:

Being insurable is generally a condition of getting a mortgage.

Already we’re seeing houses that can’t get insurance at any price thanks to natural disasters like fire, flood and cyclone, which are being accelerated by climate change.

If a buyer can’t get a mortgage, they have to pay cash.

That shrinks your potential buyer pool significantly. Which affects prices – we’d expect to see them go down, and they are.

Already $42 billion value has been lost from Australian homes from flood risk alone.

The National Climate Risk Assessment predicts a $611 billion hit to property prices. It doesn’t include the cost of fixing damage or the lost productivity from those affected having to cope and recover.

Just ask anyone who’s lived through a disaster what the long-term cost of that trauma is.

Like Clive…

Now, like most Aussies, I’m familiar with fire. I expect any Aussie reading this has seen controlled burns.

I sure did. I grew up in a leafy suburb in Brisbane called The Gap. To the west was the Brisbane Forest Park; to the north lay the Keperra bushland.

Many’s the summer when we watched the controlled burns from the Keperra direction slowly move over the hill, so I have some grasp on the sheer awe and intensity fire creates.

But watching a raging, out-of-control bushfire ravage its way towards your home is another thing entirely.

The trauma of bushfire

At the TribeFI event in Sydney earlier this month, I got to see Clive Martin speak about his experience watching a fire nearly take his home.

He’d built a beautiful home in the bush of northern New South Wales’ Tweed Shire. Mostly by hand and by himself, with the able assistance of his wife and volunteers who came to learn how to build a straw bale home. It took him five years.

He vividly described the terror of watching a bushfire come over the hill towards his (at the time, voluntarily uninsured) finished home.

Apparently he spent much of the drive out calling insurance companies for quotes and asking about waiting periods.

It was nearly lost.

The house was so well known thanks to its unique building materials and approach that the local firies dumped a water load on the fire burning in his front yard, saving the home:

That kind of trauma leaves a mark.

And it was not without financial impact. Over lunch during the event, Clive told me they had to sell the home to cash buyers.

I experienced a similar terror with flooding. There was a tremendous flood in Brisbane when I was a kid - I think it was early 1995. My mother’s car ‘drowned’ when the underground carpark running under three buildings was filled in under two hours.

I remember watching wheelie bins bobbing along the street, occasionally getting caught on the roofs of submerged cars parked there.

I have only ever bought property on high ground since.

Ask anyone who’s live through disaster - cyclone, flood and fire included. The trauma is real. It comes at personal cost to those who have to live through it and after.

Where is this happening already?

There’s an excellent case study on the PEXA site – PEXA being the digital property settlements group – about the Gippsland area, which was hit hard by the Black Summer bushfires in 2019/2020.

Cash purchases in the hardest hit eastern areas were among the highest rates of cash sales in the state.

For example, in FY24 the proportion of cash sales in three postcodes in that region – 3880, 3851 and 3909 – had cash purchases of 60.1, 51.3 and 50.8% respectively. They attribute at least part of this to buyers not being able to secure a mortgage due to risk.

The same is happening in flood-prone regions like Lismore. Cash sales rising there too.

PEXA references a report from the Actuaries Institute which mentioned 1.6m Aussies are struggling to afford home insurance already.

That’s if the insurance is even on offer.

As we’ve heard from Allianz, the point at which it’s not even on offer is coming closer. One report estimates it’ll be one in 10 properties in that situation within the decade.

Those are crap odds.

What are the flow-on effects for homes?

This will affect housing security.

With one in 10 properties potentially becoming uninsurable, Karl Mallon (chief of Climate Valuation who reported the one in 10 stat) reckons we might start seeing ‘climate ghettos’ – places where it’s hard or impossible to get insurance, so house prices go down.

But some people will have to live there simply because they can’t afford to live anywhere else.

Imagine having to live where you’re losing sleep over every weather warning, wondering if this is the time your home will be destroyed.

Not to mention unwillingness to maintain or improve properties when that threat looms large.

The vibes would suck.

If you can’t get insurance, you self-insure. Whether you plan it that way or not. So, you either roll the dice and ignore it, then get caught short if it happens to you.

Or, you put aside large amounts of cash against the day you need it.

Like, we’re talking hundreds of thousands of dollars of liquid capital, sitting there for a day that may never come, but the odds of it arriving keep getting worse.

Neither of those is ideal.

This can also put upward pressure on prices for the nine in 10 properties that remain insurable. So the ‘viable’ housing market could become even more unaffordable for the properties that are still insurable and can therefore get a mortgage.

We could see a two-tier rental market, too. Perhaps rents for more desirable (insurable) properties rising versus undesirable (uninsurable) properties falling. Adding this layer of complication to an already woeful affordability situation is worrying.

What are the flow-on effects for property investments?

This worries me for people who hold a lot property they’re planning to use as funds for retirement.

I often see people hold property till they’re getting closer to retirement, then cash in and convert the wealth to an asset that doesn’t need debt and/or is lower maintenance and/or provides a higher yield.

So what happens if you’re one of the 1-in-10 unlucky ones?

Your assets at retirement take a hit.

Then of course there’s the risk to the banks.

The mortgage books of our banks account for a lot of their shareholder value, and most of us own bank shares in some shape or form – for example, in our retirement funds or index fund shares.

Because the finance sector is such a big contributor to wealth with five of the ASX top 10 companies being banks (ANZ, CBA, Macquarie, NAB and Westpac) anything that hurts bank share price due to mortgage changes could flow through to investors holding shares.

So, for example, if the banks find themselves holding a lot of stranded assets in the residential property market, that restricts how much they can lend as they have higher risk mortgages to account for.

It’s a complicated web of regulation and the Basel III accord is the main driver here, but suffice to say: anything that significantly drops lending capacity has the potential to hit share prices.

So, you’re not immune from the effects even if you don’t own property directly.

What can we do about it?

There is no doubt in my mind:

Our best efforts should go into prevention.

Mitigation - rebadged as ‘resilience’ - will have to happen too. But we’ll need less resilience if we can slow or stop climate change, given its impact on the frequency and severity or extreme weather events.

So: prevention first.

It starts with a swifter transition away from fossil fuels.

You’ll find out how you can help in the ‘Move APACE’ blogs. Spoiler alert: it involves moving your money.

We also have to acknowledge that we’re already on this path.

Australia’s at 1.51 degrees of warming today.

Insurance is unavailable for some homes today.

This is already happening.

If the world acts ambitiously – Aussies included – we might be able to stop at peak warming of 1.7 degrees if we take the ‘highest ambition’ path.

But the current trajectory has us going past 2.5 degrees, so it’s only going to get much worse if we don’t act swiftly enough.

So, what can an individual do after the Move APACE options?

Add the climate impact layer to your property decision making

The golden rule in property has always been:

Location, location, location.

But it’s not just proximity to schools and ocean views you need to worry about now.

You need to consider climate risks too.

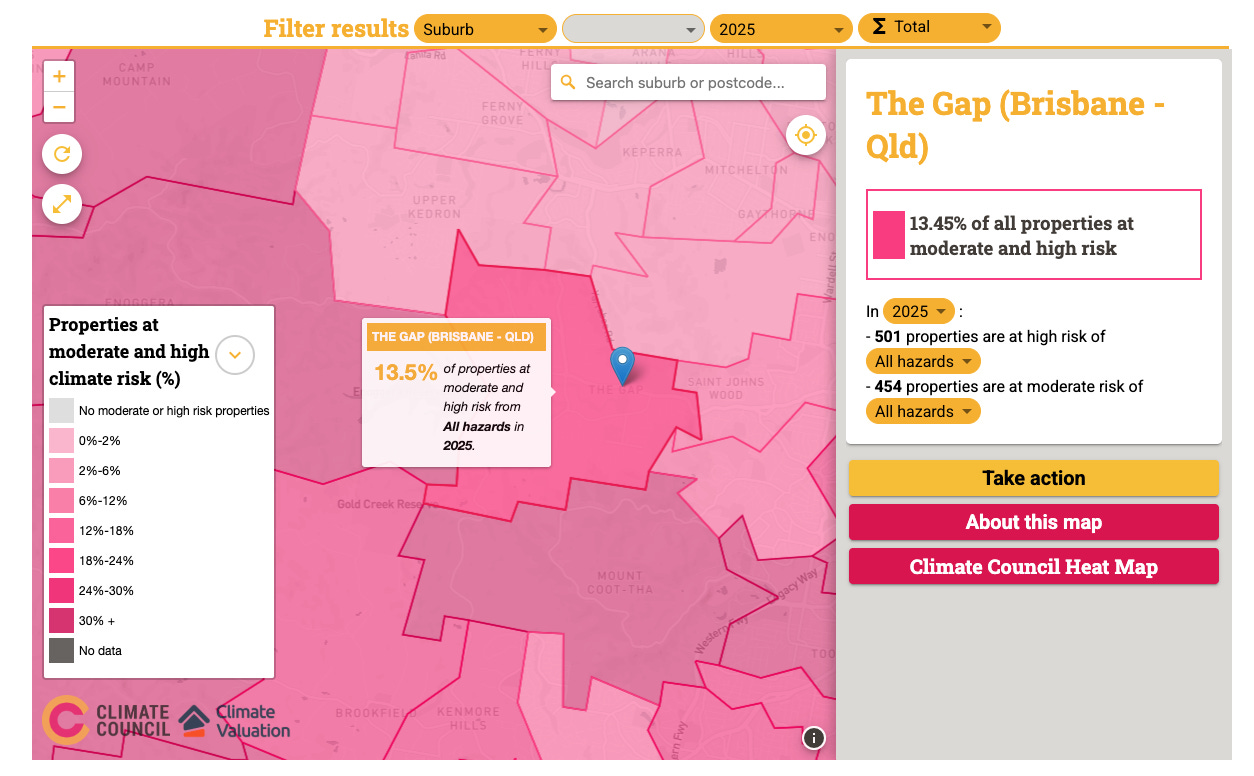

You can check the Climate Council’s Climate Risk Map to see what risks your postcode is projected to have insurance wise now, in 2050 and in 2100, and what the major threat is.

For example, my old home base, The Gap QLD has 13.45% of homes at moderate to high risk of all hazards in 2025:

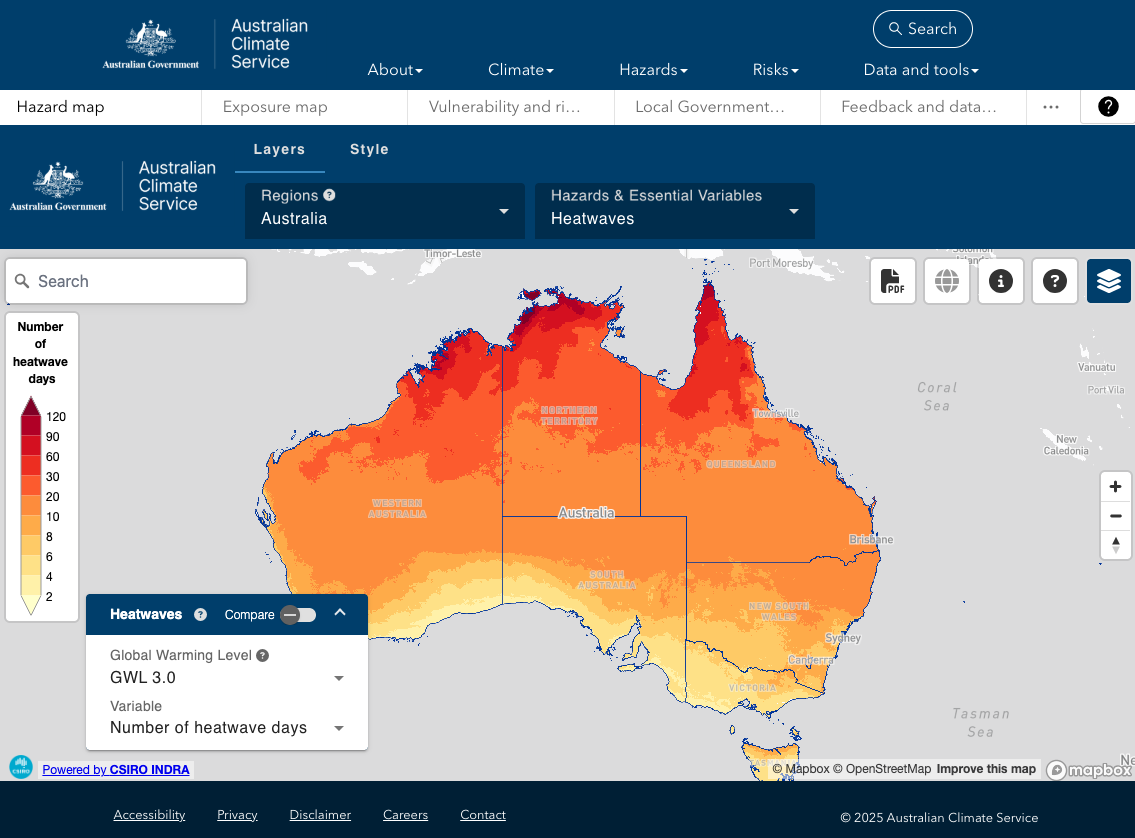

There’s an Australian Climate Service data explorer to visualise risk too:

If an area you’re considering has risk you find unacceptably high, you might want to rethink the purchase.

If you’re already an owner, you might want to think about protection.

For example, if it’s a fire risk area, do you want to install a fire suppression system, or any other fire defence equipment?

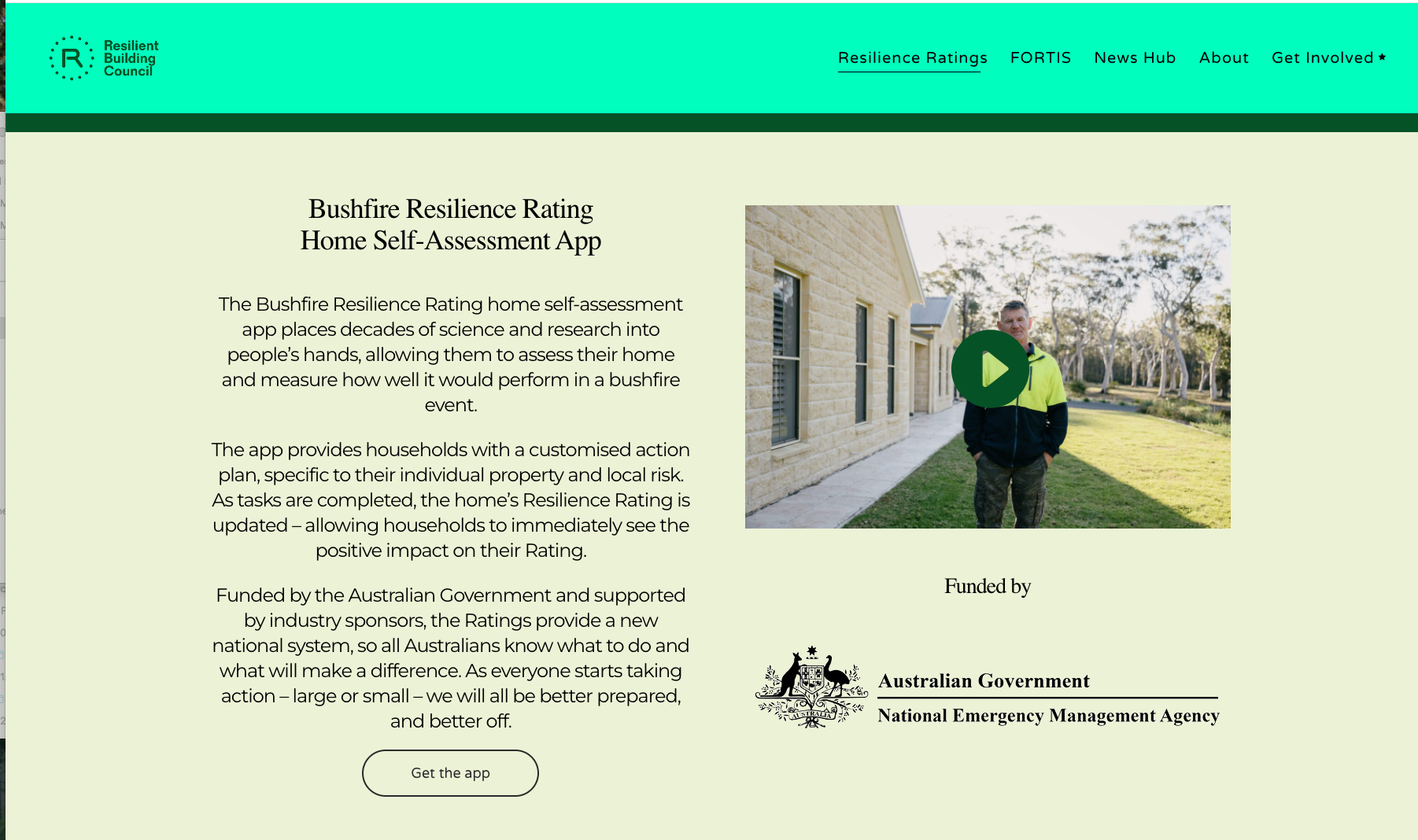

There’s an excellent resource on climate adaptation called Resilient Building Council. You can try their home self-assessment app and see what they recommend for improving your home:

And there are certainly people building homes designed to withstand disaster.

Take this couple who built a home on the banks of the Brisbane River.

It’s designed to recover from flooding – a ‘house you can hose out’. Great episode of Grand Designs if you like that kinda thing. It costs a pretty penny, but it’s an option if you’ve got the wealth behind you.

I just wonder what it’s like to be the only house of its kind on your stretch of the river? Is it still worth building and living there if all your neighbours abandon the area anyway?

There are also service providers offering to vet your property investments, and the banks have tools too – for example, Suncorp’s Haven.

They might also be useful.

Okay, that’s property.

Now onto the bit that affects most Australians through their retirement funds: shares…