Shares won't escape the fallout if climate change runs riot

Contrary to what many experts seem to believe, property's not the only asset class with exposure to climate change risks. Shares are on the line too.

The link between climate change and property is explicit and obvious.

More frequent and intense disasters threaten to burn, flood or blow away more buildings. Insurance can’t sustain coverage.

The link to shares may seem less obvious, until you connect the dots between production and share price.

Which BlackRock quietly did in January 2025.

If you haven’t already read it, their investment stewardship paper on the topic is just four pages. Take a squiz.

As you’ll see, the main points are:

55% of global production is moderately or heavily dependent on nature.

Global markets have not fully priced in the risks to nature.

As well-respected economist and public servant Dr Ken Henry stated in several recent addresses, including to the National Press Club, the National Environmental Law Association Conference and in conversation with Curtin MP Kate Chaney:

There is no contest between nature and economy.

You cannot have an economy without nature. If we want a thriving economy, we must rebuild nature. But I’m jumping ahead of myself, into the realm of solutions.

If we don’t rebuild nature, what might happen to wealth we’ve got in shares?

Pricing today might not reflect tomorrow

As the BlackRock paper says (bolding mine):

“BlackRock’s research shows that only a portion of natural capital’s value to the economy is priced into markets today. This analysis suggests asset prices could adjust to better reflect both the risks and opportunities linked to natural capital, driven in large part by increasing physical risks.”

So look, there’s *a chance* the price of a given company’s share could increase according to BlackRock.

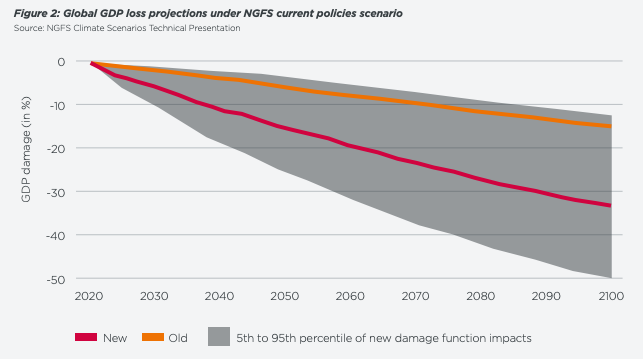

…but given The Institute and Faculty of Actuaries and University of Exeter’s Planetary Solvency Report showing old modelling has seriously underestimated gross domestic product (GDP), share price dropping seems more likely on average:

The big risk to you as an investor is that you pay more than a share is really worth.

For example, it might be overpriced because the market hasn’t worked out:

how much production is likely to drop due to climate change worsened impacts on nature.

whether the company could find some or all of its assets stranded (please see this excellent brief explainer from the Australasian Centre for Corporate Responsibility, ACCR).

On the stranded assets piece, take coal mining.

Ever since the International Court of Justice issued its Advisory Opinion on Climate Change, the legal system now has more pressure not approve fossil fuel projects.

I mean, it could be coincidence that an approval for a massive coal mine in the Hunter Valley was overturned within 12 hours of the ICJ’s statement. But that’d be a pretty wild coincidence?

So, what does MACH Energy - the Indonesian company who applied for and thought they had the approval - do with that lease now?

It’s not worth much to other coal miners if the government won’t approve more mining.

Chances are it’s either already stranded, or it’s on its way.

Brace for balance sheet write-downs incoming.

In this case, MACH Energy appears to be privately owned. So, no retail shareholders like us were harmed in the making of this story. But you catch my drift here.

If you’re caught holding shares in a company who turns out to be much less productive than the share price used to suggest, you can kiss some of your share value goodbye.

And not just in your direct share holdings. Brace for impact to your retirement fund too.

How does this also hit retirement funds?

You might see just one investment choice in your superannuation fund. It’s often branded something cute like ‘Balanced’ or ‘MySuper’ or ‘Socially Conscious’. Excellent marketing tactics, those names.

Anyway, you hold X many units of it. The price of those units goes up and down, and that’s what sets the balance of your super fund.

Each unit is backed by the assets the super fund bought with your money.

Super funds tend to have shares as part of their holdings. Any downward movement of those holdings will eventually flow into your super balance.

Now, all shares are in the mix when it comes to that 55% GDP linkage to nature. But most mainstream MySuper products are exposed to two very obvious potential sector hits:

1. Banks

Banks are a big part of the Australian economy, comprising five of our 10 biggest companies on the ASX.

If you have direct shares in a bank, indirect shares through your super or an index fund like an ETF or LIC, you have exposure to the banks and therefore the property market. Even if you don’t own property.

If property takes a hit, that can flow through to the banks’ mortgage books, then revenue, and therefore hit share price.

If more mortgages turn out to be riskier too, the banks have to hold more capital due to regulation. That reduces their lending capacity, which again hits revenue, then share price.

2. Fossil fuel companies

Most MySuper investment mixes hold shares in fossil fuel producers. With courts rescinding approvals for coal mines, assets that cause the climate change killing nature are at greater risk of stranded assets. This makes their share price subject to risk too.

How big an impact are we talking?

There’s one report predicting up to 50% contraction of GDP by 2070 to 2090.

That’s quite a range, I know. Such is the nature (ha!) of this modelling.

Unfortunately with climate change, a lot of stuff is happening quicker than modelled, so we can’t be confident on the timing or the magnitude.

But just to put that into perspective: global GDP dropped 3.2% during COVID.

Remember how much life was when we had to reprioritise all efforts towards basic needs like food, water, shelter? It wasn’t great, right? No cures for cancer being researched if we end up in a more permanent GDP contraction.

Even a small contraction of GDP would affect our quality of life negatively. And it’ll affect your wealth, also negatively.

But aren’t super funds self-correcting?

…and while we’re at it, what about exchange-traded funds (ETFs) and listed investment companies (LICs), who also hold a portfolio of companies on the shareholders’ behalf?

They are self-correcting in some cases, because they buy and sell shares based on the ranking on the sharemarket along with other metrics each fund applies. As a company drops out of the Top 100, 200 or whatever number they’ve set as their remit, they are sold and replaced if it’s a straight market-tracking fund.

Certainly, they’re more self-correcting than if you own direct shares in a fossil fuel company or a bank.

But when there’s less production all round, wealth has to contract eventually. You can’t resilience your way out of this unfortunately.

Then you have BlackRock’s point about pricing – that these risks aren’t accurately reflected in asset pricing right now - as mentioned above. BlackRock’s changing their pricing, but are all the super funds and ETF/LIC providers?

Especially anyone holding fossil fuel companies, which might see stranded assets hit share price sooner rather than later.

So, what can we do?

Again - and I know I’m repeating myself ad nauseum, but I’m gonna keep doing it - the best case scenario is we slow or stop climate change.

Specific fixes for you to consider are coming in the Move APACE posts.

The next thing is to pay careful attention to what you’re holding, including the underlying assets if it’s retirement or index funds.

Thanks to disclosure requirements, it’s all very easy to search these days.

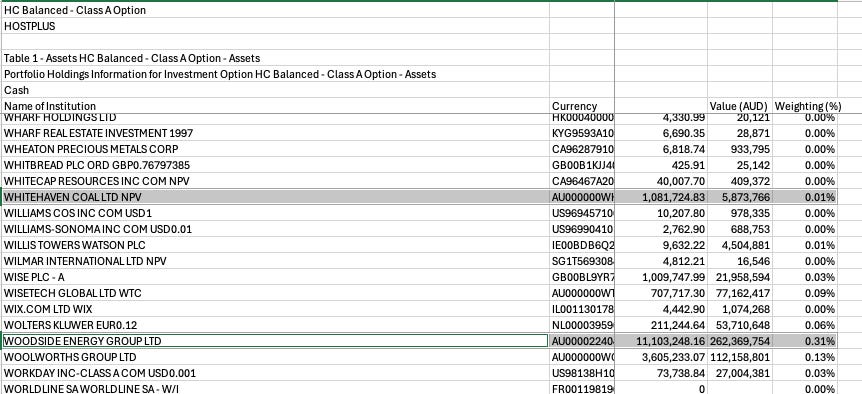

Just pop the name of the investment mix or ETF/LIC into your preferred search engine and you’ll find the list. Like this - I’ll do Barefoot’s favourite fund, Hostplus, but look at their most popular investment, the MySuper Balanced fund:

Check what it’s holding and make sure you’re happy with it.

In my case, I’m avoiding ETFs, LICs and super that hold fossil fuel companies because of that stranded asset risk, as well as not wanting to facilitate shrinking my wealth!

I’ll go into more detail on this in the Move APACE posts, but before I do…

You might be wondering: why aren’t we hearing about this in mainstream media? I have theories…